CMS just locked in a 2.48% payment increase – far higher than anyone expected. Here’s what it means for your premiums, your benefits, and your choices this fall.

If you’re one of the more than 35 million Americans enrolled in a Medicare Advantage plan or if you’re about to turn 65 and weighing your options — the 2027 rate announcement from the Centers for Medicare & Medicaid Services is news that directly touches your wallet, your benefits, and your peace of mind.

On April 6, 2026, CMS dropped a number that surprised practically everyone: a 2.48% average rate hike for Medicare Advantage (MA) plans in Calendar Year 2027. That’s a 27-fold jump from the measly 0.09% that the agency floated back in January and it translates into more than $13 billion in additional government payments flowing to MA insurers next year. If you had seen health insurer stocks – UnitedHealth and CVS Health each jumped more than 9% in after-hours trading, while Humana surged around 12%, you already sensed the significance.

But what does any of this mean for you, sitting at your kitchen table trying to figure out whether your dental coverage will still be there in 2027? Let’s break it all down plainly, honestly, and without the Washington jargon.

What is the Medicare Advantage Rate Hike for 2027?

Every year, CMS – the federal agency that runs Medicare, sets the payment rates it will use to reimburse private insurance companies for running Medicare Advantage plans. Think of it as the government’s annual check to companies like Humana, UnitedHealthcare, Aetna, and CVS Health in exchange for providing Medicare coverage to their enrollees.

The 2027 final rate announcement, officially released on April 6, 2026, finalizes a net average payment increase of 2.48% or more than $13 billion above what the government was paying plans in 2026. When you factor in the estimated trend in MA risk scores (driven by population changes and coding practices), the effective increase reaches a full 4.98%.

From Panic to Relief: How the Final Number Jumped So Much

The story of the 2027 rate is really the story of two very different numbers. In January 2026, CMS published its Advance Notice proposing just a 0.09% increase — barely above zero. Industry analysts described it as a near-catastrophe. Insurance companies warned they’d have to slash benefits, hike premiums, or exit entire markets. The Better Medicare Alliance, a major advocacy organization, mobilized thousands of beneficiaries to flood CMS with public comments.

By the time the final number landed in April, the story had flipped. CMS walked back its proposed risk adjustment model recalibration — the single biggest driver of the original low figure and incorporated updated Medicare claims data through Q4 2025. The result: a 2.48% final increase that Wall Street cheered and patient advocates quietly welcomed, even if the insurance industry had hoped for closer to 3–5%.

Breaking Down the 2027 Medicare Advantage Payment Changes

The final rate announcement is more than just one headline number. It’s a collection of interlocking policy decisions, each of which shapes how much money flows to plans and ultimately to beneficiaries. Here’s what’s actually inside the 2027 announcement.

1. The Effective Growth Rate

This is the backbone of the rate increase. The Effective Growth Rate reflects projected growth in Medicare Advantage benchmarks, largely driven by growth in Original (Traditional) Medicare per capita costs as estimated by CMS’s Office of the Actuary. The incorporation of updated program experience data including original Medicare claims through Q4 2025 – significantly lifted the growth rate from what was initially proposed in January.

2. The Risk Adjustment Model: A Major Reversal

This was the most controversial element of the 2027 cycle. In January, CMS had proposed updating the risk adjustment model with far more recent data — shifting from calibration based on 2018 diagnoses and 2019 expenditures to 2023 diagnoses and 2024 expenditures. Insurers argued this would dramatically reduce their payments and they hadn’t had enough time to absorb the Biden-era V28 model changes that were just fully phased in.

CMS listened. For 2027, the agency will continue using the 2024 MA risk adjustment model calibrated with the older data, giving the market more time to adjust. Industry analysts called the reversal “hard to overstate” as a victory for the MA sector.

3. Excluding Diagnoses From Unlinked Chart Review Records

Not everything went the industry’s way. CMS did finalize a meaningful anti-upcoding measure: starting in 2027, diagnoses from unlinked Chart Review Records (CRRs) – records not tied to an actual patient encounter will no longer count toward risk scores. There is one exception: beneficiaries switching from one MA organization to another.

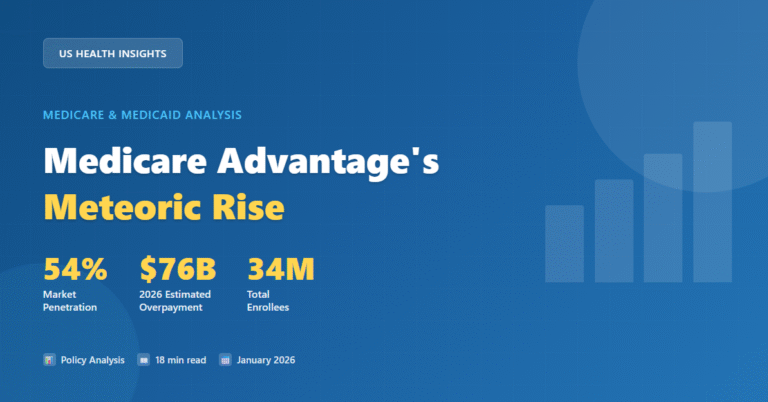

This matters because upcoding where insurers submit diagnoses that make patients appear sicker than they are to collect higher risk-adjusted payments has been estimated to cost taxpayers tens of billions of dollars annually. The Medicare Payment Advisory Commission (MedPAC) recently found that MA costs the government $76 billion more per year in 2026 compared to a scenario where all beneficiaries were in Traditional Medicare.

4. Star Ratings and Quality Bonus Payments

The 2027 payment rates incorporate 2026 Star Ratings for quality bonus payments. Plans that earn four or more stars receive meaningful payment bonuses — which in turn often fund the richer benefits (like dental, vision, and fitness) that attract enrollees to MA in the first place. CMS also finalized a major Star Ratings overhaul in early April 2026, which is expected to send billions of additional dollars to higher-performing plans over the next decade.

5. Part D Risk Adjustment Updates

The 2027 announcement also covers Medicare Part D — prescription drug coverage. CMS finalized updates to the Part D risk adjustment model that account for changes under the Inflation Reduction Act, reflect more current costs, and separately account for MA-PD (prescription drug plans bundled with MA) and standalone PDP costs. These changes are designed to bring greater stability to drug benefits for all Medicare beneficiaries.

| Payment Component | Proposed (Jan 2026) | Final (Apr 2026) | Direction |

|---|---|---|---|

| Net Average Payment Increase | 0.09% (~$700M) | 2.48% (~$13B+) | Significantly Higher |

| Effective Increase (incl. risk scores) | 2.54% | 4.98% | Higher |

| Risk Adjustment Model Recalibration | Proposed (2023 data) | Withdrawn (2018 data retained) | Favorable for Plans |

| Unlinked CRR Diagnoses Excluded | Proposed | Finalized (with exception) | Anti-upcoding measure |

| Part D Risk Adjustment Update | Proposed | Finalized | More accurate drug pricing |

What Does the 2027 Rate Hike Mean for Medicare Beneficiaries?

Here’s where it gets personal. The rate hike affects insurers directly but its ripple effects reach every person holding a Medicare Advantage card. Here’s what you should actually be thinking about.

Will My Premiums Go Up or Down in 2027?

The short answer: the 2.48% increase is a positive signal for premium stability, but it doesn’t guarantee your specific plan’s premiums won’t rise. Government payment rates are one input into what insurers charge – medical utilization trends, local market competition, and plan-specific Star Ratings all matter too.

Before the final rate was announced, AHIP (the major health insurer trade group) commissioned a study projecting that if the nearly flat 0.09% rate had been finalized, the typical senior couple would face a premium increase of $23/month – over $550/year. That worst-case scenario is now off the table. But industry groups note that 2.48% still doesn’t fully keep pace with the actual cost pressures facing insurers and the physicians they contract with.

What About My Extra Benefits – Dental, Vision, Hearing?

This is the question most beneficiaries care about most. Over the past two years, many MA enrollees experienced benefit cuts in dental, vision, over-the-counter allowances, and fitness programs as insurers trimmed costs in response to elevated medical utilization after the pandemic. The 2.48% final rate takes some pressure off but it does not guarantee a return to the richer benefit packages of 2022 and 2023.

Analysts at Mizuho noted that the boost may help companies expand margins in 2027 — if they keep reducing benefits and managing expenses. In other words, the extra money could go to shareholder returns as easily as it goes back to your dental plan. Watch your Annual Notice of Change carefully when it arrives in the fall.

Action Step for Beneficiaries:

Every year, MA plans must mail you an Annual Notice of Change (ANOC) by September 30. This document will spell out exactly what’s changing in your plan for 2027 – premiums, copays, deductibles, and covered benefits. Read it. Don’t file it away. The Annual Enrollment Period (AEP) runs October 15 – December 7, giving you the window to switch plans if yours is cutting benefits.

Will My Plan Still Be Available in 2027?

Plan exits were a major concern heading into the 2027 cycle. Most major insurers trimmed their MA membership going into 2026, sacrificing growth for profitability. CMS officials acknowledged they weighed the risk of coverage disruptions for seniors – especially with November 2026 midterm elections approaching – when setting the final rate. The more generous 2.48% figure is intended, in part, to reduce the incentive for plans to exit underperforming markets.

Rural Beneficiaries: Still at Greater Risk

Under the original 0.09% proposal, AHIP research found that approximately 70% of MA beneficiaries lived in counties projected to experience payment cuts, with rural communities facing the steepest reductions. The final 2.48% rate relieves much of that pressure but rural access remains a structural challenge, with fewer competing plans and thinner provider networks already in place.

The Bigger Picture: Is Medicare Advantage Still Worth It in 2027?

Medicare Advantage covers more than half of all Medicare beneficiaries – a landmark crossed in 2025. The program’s appeal has always been the combination of lower monthly premiums and extra benefits not available in Original Medicare. But the program has faced mounting scrutiny over the past few years, driven by three overlapping concerns.

The Overpayment Problem

MedPAC’s finding that MA costs the government $76 billion more per year than Traditional Medicare — largely due to coding practices — is not a partisan talking point. It’s a bipartisan fiscal concern that both CMS administrators under both parties have tried, with varying success, to address. The exclusion of unlinked Chart Review Records in 2027 is a step in the right direction, but critics argue the structural incentives to upcode haven’t been eliminated.

The Benefit Volatility Problem

The past two enrollment cycles exposed a growing vulnerability in MA: supplemental benefits (dental, vision, OTC allowances) can disappear year to year. Unlike Original Medicare, where covered benefits are set by federal law and don’t change annually, MA benefits are determined by what plans choose to offer — and what the government payment rate will sustain. This volatility has prompted some seniors to reconsider whether the extra benefits are worth the uncertainty.

The Access Problem

Prior authorization requirements, narrow networks, and treatment denials have drawn congressional scrutiny. CMS’s 2027 reforms include a new special enrollment period trigger: beneficiaries will be able to switch plans outside of open enrollment when their provider exits an MA network — even without CMS having to determine whether the departure was “significant.” That’s a small but meaningful improvement in consumer protections.

Original Medicare vs. Medicare Advantage: A Quick Comparison for 2027

Original Medicare (Parts A & B): Federal program with set benefits, freedom to see any Medicare-accepting provider nationwide, no annual cap on out-of-pocket costs without a Medigap supplement, predictable year-to-year coverage.

Medicare Advantage (Part C): Private plans covering A, B, and usually D; often lower premiums; extra benefits like dental, vision, and hearing; but network restrictions, prior authorization requirements, and year-to-year benefit variability.

Bottom line: There’s no universal answer. It depends on your health status, your doctors, your finances, and your tolerance for plan changes. The 2027 rate hike slightly tilts the MA calculus in a more favorable direction but the structural trade-offs remain.

How the 2027 Rate Compares to Recent Years

| Plan Year | Proposed Rate | Final Rate | Additional Payments |

|---|---|---|---|

| 2025 | ~3.7% | ~3.7% | ~$16B |

| 2026 | 2.2% | 5.06% | ~$25B |

| 2027 | 0.09% | 2.48% | $13B+ |

The pattern of CMS proposing a low number and then finalizing a much higher one is becoming notable. For 2026, the gap between proposal and final was nearly 3 percentage points. For 2027, it was even wider in relative terms – from a near-zero proposal to a 2.48% final rate.

5 Smart Steps Every Medicare Beneficiary Should Take Before 2027

- Read your Annual Notice of Change (ANOC) in September 2026. This is the document that tells you exactly what your plan is changing. Don’t let it sit unopened on a table.

- Log on to Medicare.gov’s Plan Finder during the Annual Enrollment Period (Oct. 15 – Dec. 7, 2026). Compare your current plan to alternatives in your ZIP code. Drug formularies, network doctors, and out-of-pocket maximums can vary significantly even within the same insurer family.

- Check your plan’s Star Rating. Higher-rated plans (4–5 stars) tend to be more financially stable, have better member satisfaction, and often provide richer benefits. CMS publishes Star Ratings each fall at medicare.gov.

- If you have a specialist you can’t afford to lose, verify they’re in-network — every year. Provider networks can change annually. Don’t assume your cardiologist or oncologist will still be in your plan’s network just because they were last year.

- Talk to a licensed Medicare counselor (SHIP). Every state has a free State Health Insurance Assistance Program (SHIP) that offers one-on-one, unbiased Medicare counseling. They can help you compare plans without trying to sell you anything.

Don’t Wait Until Open Enrollment to Get Informed

The 2027 Medicare Advantage rate announcement is decided but how it affects your specific plan, your premiums, and your benefits won’t be clear until fall 2026. Start preparing now so you can make a confident choice during the Annual Enrollment Period. Compare Plans at Medicare.gov.

Frequently Asked Questions

1. What is the Medicare Advantage rate hike for 2027?

CMS finalized a net average payment increase of 2.48% for Medicare Advantage plans in Calendar Year 2027, announced on April 6, 2026. This adds more than $13 billion in government payments to MA plans compared to 2026. When accounting for estimated risk score trends due to population changes and coding practices, the effective increase reaches 4.98%.

2. Will Medicare Advantage premiums go up in 2027?

The higher-than-proposed final rate reduces upward pressure on premiums. However, individual plan premiums depend on many factors beyond the government payment rate — including local medical costs, the plan’s Star Rating, competition in your market, and insurer decisions about benefit design. Your specific premium changes will be announced in your Annual Notice of Change, which plans must send by September 30, 2026.

3. When will 2027 Medicare Advantage plan details be available?

MA plans submit their 2027 benefit designs to CMS over the summer of 2026. Official plan details become publicly available when the Annual Enrollment Period opens on October 15, 2026. You can compare plans at Medicare.gov’s Plan Finder. Plans must also mail you an Annual Notice of Change by September 30, 2026.